2026 is the year stablecoin settlement crossed the chasm. Visa announced live USDC settlement to merchant acquirers in Q1. Stripe re-launched its crypto payouts feature in ten new countries. Mastercard's Multi-Token Network expanded to include USDC and EURC. And on the merchant-facing side, a new generation of stablecoin payment gateways made it possible for any business — high-risk or not — to accept cards and settle in dollar-pegged crypto, instantly, with no bank dependency.

This guide walks through the why and the how: why stablecoin settlement structurally beats fiat settlement for merchants, why USDC has emerged as the default stablecoin, why Polygon dominates as the settlement chain, and which verticals see the biggest revenue lift from making the switch.

1. Introduction: The Stablecoin Inflection Point

For the first 30 years of e-commerce, "getting paid" meant: customer pays by card → acquirer settles into a merchant account → merchant withdraws to a bank account. Every step was governed by a different intermediary, each with its own risk policy, each with the power to interrupt the flow. For low-risk, US-based merchants this chain mostly worked. For everyone else, it was unstable by design.

Stablecoins broke the chain. By replacing the merchant-account → bank-account leg with an on-chain transfer of USDC, three things happen at once:

- The merchant has no account that can be frozen.

- Settlement is instant, irreversible, and globally available.

- The chargeback risk is contained to the fiat-acquirer side, not the merchant.

What used to take 2-7 days and pass through 3 intermediaries now takes 2 minutes and passes through 1. That's the inflection point.

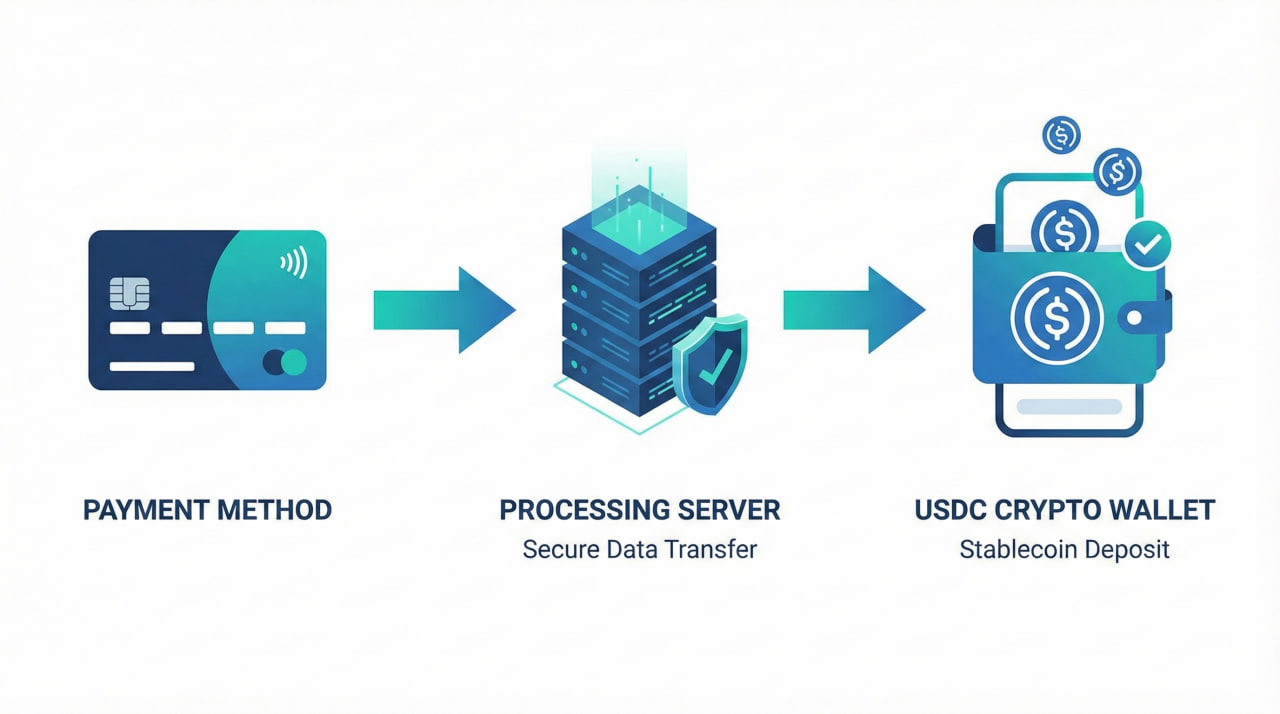

2. What Is a Stablecoin Payment Gateway?

A stablecoin payment gateway is a payment processor that accepts traditional fiat payment methods (cards, mobile wallets, bank transfers) and settles the merchant's share in a dollar-pegged stablecoin like USDC instead of in fiat currency. From the customer's perspective, the experience is identical to any modern card checkout. From the merchant's perspective, the back-end settlement model is fundamentally different.

The flow:

- Customer pays $49.99 with Visa, Mastercard, Apple Pay or Google Pay.

- The fiat side of the transaction is processed by a licensed acquiring partner — same card networks, same 3D Secure 2 flow, same fraud screening as Stripe or PayPal.

- The gateway converts the merchant's portion to USDC at the spot rate (typically $1 = 1 USDC, with a sub-cent spread).

- USDC is sent on-chain to the merchant's wallet within minutes.

- The merchant's WooCommerce / WHMCS / custom store marks the order as paid.

The customer never sees the stablecoin. They never interact with a wallet. They never need to know what Polygon is. The stablecoin layer is entirely invisible to them — it only matters on the merchant side, where it eliminates the bank dependency.

For a deeper breakdown of the card-to-crypto pattern in general, see Best Card-to-Crypto Payment Gateway and the wallet-only setup pattern in Accept Payments Without a Bank Account.

3. Why Stablecoin Settlement Beats Fiat for Merchants

Five structural reasons make stablecoin settlement strictly better than fiat for merchants in 2026:

1. No Merchant Account, No Account Freeze Risk

The biggest single risk in fiat processing is the merchant account itself. Stripe, PayPal, Square and every other traditional processor reserves the right to freeze funds for 90-180 days at any time, with or without cause. A stablecoin gateway settles directly to your wallet — there is nothing for a risk team to freeze retroactively.

2. No Rolling Reserves

Traditional high-risk processors hold 5-10% of every transaction in reserve for 6 months. On $50K/month in revenue that's $25K-$50K of your own working capital permanently parked. With stablecoin settlement, 100% of every approved transaction arrives in your wallet within minutes.

3. Instant, Irreversible Settlement

USDC arrives within minutes. The transaction is verifiable on PolygonScan. There is no T+1, no T+5, no weekly batch — the moment the card payment is approved, the stablecoin is on its way.

4. Global by Default

Stablecoins are not bound by territorial banking. A merchant in Argentina accepting a card from a customer in France settles the same way a merchant in Singapore accepting a card from a customer in Brazil does. No correspondent banking, no SWIFT, no cross-border fees beyond network gas (~$0.01 on Polygon).

5. Chargeback Liability Is Bounded

On the customer side, chargebacks still exist (the cardholder can dispute through Visa/Mastercard). But the chargeback liability is contained at the acquiring partner — the merchant's wallet has already been credited with USDC. This decouples cash-flow predictability from chargeback timing. For an in-depth take, see Chargeback Prevention for High-Risk Merchants and Best Payment Gateway Without Chargebacks.

4. USDC vs USDT: Which Stablecoin to Settle In

The two dominant dollar-pegged stablecoins are USDC (Circle) and USDT (Tether). Both are pegged 1:1 to the US dollar, both have multi-billion-dollar market caps, both trade at near-perfect parity. The differences matter when you're a merchant accumulating treasury balance.

USDC — Circle (Recommended for Merchant Settlement)

- Issued by Circle Internet Financial, a regulated US fintech.

- 1:1 reserves in cash and short-term US Treasuries.

- Monthly reserve attestation by a Big Four auditor (Deloitte).

- Compliant with US sanctions list (OFAC) — addresses can be frozen for OFAC hits, but not for routine merchant volume.

- Strong banking relationships (BNY Mellon, BlackRock-managed treasury).

USDT — Tether

- Issued by Tether Limited, a Hong Kong-based offshore company.

- Reserves disclosed quarterly, attested but not full audit.

- Reserve composition includes corporate paper, secured loans, and other assets beyond cash and Treasuries.

- History of regulatory action (NYAG settlement, CFTC fine).

- Largest market cap, deepest liquidity, but higher tail risk.

For a merchant settlement default, USDC is the lower-risk choice. That's why Chain2Pay uses USDC as the canonical settlement currency. Merchants who specifically need USDT can convert post-settlement at any DEX (Uniswap on Polygon handles USDC↔USDT conversion at near-zero spread).

5. Polygon vs Ethereum: Which Chain to Use

USDC exists on multiple blockchains. The two that matter for merchant settlement are Polygon and Ethereum mainnet. Each has trade-offs.

Polygon (Recommended for Most Merchants)

- Gas fees: ~$0.01 per transfer.

- Block time: ~2 seconds.

- Final settlement: 1-2 minutes.

- USDC liquidity: $1B+, Circle-native.

- Ecosystem: 200+ integrations, every major wallet supported.

Ethereum Mainnet

- Gas fees: $5-$50 per transfer (varies with network load).

- Block time: ~12 seconds.

- Final settlement: 3-5 minutes.

- USDC liquidity: $40B+, Circle-native.

- Ecosystem: deepest, most institutional, most expensive.

For 99% of merchants, Polygon is the right choice. The gas savings alone make a meaningful difference at scale: a merchant processing 10,000 transactions/month saves $50K-$500K/year on gas vs Ethereum mainnet, with zero functional downside.

Ethereum mainnet only makes sense if your treasury operations are entirely on L1 (DeFi integrations, institutional custody, etc.) — and even then, the typical pattern is to settle on Polygon and bridge to Ethereum in batches.

6. Verticals That Benefit Most

Every merchant benefits from instant USDC settlement, but a few verticals see outsized returns from making the switch:

- High-risk merchants (IPTV, CBD, casino, forex, adult, peptides, digital keys, SaaS): The merchant-account-freeze risk drops to zero. See our top 5 roundup.

- Global / cross-border merchants: No more correspondent banking or FX losses on incoming cards. USDC settles the same way regardless of customer country.

- Subscription businesses: Cash-flow predictability is dramatically better when 100% of approved revenue arrives within minutes.

- Crypto-native businesses: Already operate in stablecoins for treasury — settling in USDC eliminates the fiat-to-crypto conversion step.

- Emerging market merchants: In Argentina, Turkey, Nigeria, Lebanon and similar high-inflation economies, settling in USDC instead of local currency preserves purchasing power.

For trends and what's next in this space, see our forward-looking high-risk payment gateway trends 2026 article.

7. Frequently Asked Questions

What is a stablecoin payment gateway?

A stablecoin payment gateway accepts traditional payment methods (Visa, Mastercard, Apple Pay, Google Pay) and settles the merchant's portion in stablecoins like USDC instead of fiat currency. The customer pays in their local currency; the merchant receives a dollar-pegged stablecoin within minutes.

Why is USDC preferred over USDT for merchant settlement?

USDC is fully reserved 1:1 in cash and short-term US Treasuries, with monthly reserve attestation by a Big Four auditor (Deloitte), and issued by Circle (a regulated US fintech). USDT (Tether) has a more opaque reserve composition and a history of regulatory pressure. For merchants, USDC is the lower-risk default.

Is a stablecoin payment gateway better than Stripe for high-risk merchants?

For high-risk verticals (IPTV, CBD, casino, forex, adult, peptides, etc.), yes — by a wide margin. Stripe will eventually freeze high-risk accounts; a stablecoin gateway settles directly to a non-custodial wallet, eliminating the freeze risk entirely.

Can my customers pay without knowing it's a stablecoin on the backend?

Absolutely. Customers see a standard card checkout. They enter card details (or use Apple Pay / Google Pay) and never interact with crypto. The stablecoin layer is invisible — only the merchant sees USDC arriving in their wallet.

What chain does Chain2Pay's stablecoin gateway settle on?

Polygon by default. Polygon offers ~$0.01 gas fees, ~2-second block times, and full USDC liquidity. Settlement is verifiable in real-time on PolygonScan. Chain2Pay can also support Ethereum mainnet for merchants who specifically need it.

Are stablecoin payment gateways legal?

Yes. The fiat (card) leg is processed by licensed acquiring banks subject to standard regulations. The merchant's settlement in USDC is a standard crypto transfer subject to crypto-asset rules in the merchant's jurisdiction.

8. Conclusion

The shift from fiat settlement to stablecoin settlement is one of those transitions that looks gradual until it doesn't. Visa, Mastercard and Stripe all moved decisively in 2025-2026. The merchant tools caught up. The gas costs collapsed (Polygon). The regulatory clarity on USDC matured. What used to feel experimental now feels like infrastructure.

For high-risk merchants, the value proposition is overwhelming: cards in, USDC out, no merchant account anyone can freeze, no rolling reserve eating into working capital. For global merchants, it's the simplest way to receive money from any country without SWIFT or correspondent banking. For everyone else, it's a faster, cheaper, more predictable settlement layer than fiat.

Chain2Pay is one of the cleanest implementations of this stack in 2026: card checkout, USDC on Polygon, instant settlement, no KYC for the merchant. Move your gateway, move your treasury, get back to running your business.