1. Introduction

In 2026, high-risk merchants are still facing the same problem they did five years ago: Stripe, PayPal and Square ban their accounts without warning, freeze their revenue for 90 to 180 days, or refuse them outright at the application stage. The reasons rarely have anything to do with fraud — selling subscriptions, digital goods, IPTV streams, adult content or anything in a regulated vertical is enough to trigger an automatic decline.

The good news is that a new generation of crypto-backed gateways has rewritten the rules. By settling instantly in stablecoins like USDC instead of routing funds through a fragile merchant account, these processors give high-risk businesses something they never had with Stripe or PayPal: payment infrastructure that can't be turned off overnight.

In this guide we compare the 5 best high-risk payment gateways available right now — covering card-to-crypto solutions, traditional high-risk processors and crypto-only gateways — so you can pick the one that actually fits your business model.

2. What Makes a Payment Gateway High-Risk

A "high-risk" classification has nothing to do with the legitimacy of your business — it's a risk-scoring decision made by acquiring banks based on a handful of structural criteria. If your business hits any of these, traditional processors will treat you as high-risk by default:

Elevated Chargeback Ratios

Anything above the Visa 0.9% / Mastercard 1% chargeback threshold puts your account in the high-risk bucket. Subscription billing, intangible goods and impulse purchases all push this ratio up structurally.

Intangible Products & Recurring Billing

Software licenses, IPTV access, SaaS subscriptions, digital downloads — anything that can't be physically returned creates dispute resolution headaches that acquirers prefer to avoid entirely.

International Customer Base

Selling in 30+ countries with mixed currencies, varied regulatory environments and cross-border card networks is a textbook high-risk profile in the eyes of US/EU acquirers.

Regulated Industries

IPTV, adult content, online gambling, forex, crypto services, CBD/cannabis and a long list of other verticals are systematically rejected by tier-1 processors regardless of revenue or compliance posture.

Industry reality: Stripe's own ToS lists more than 30 prohibited business categories. PayPal lists 25+. If you operate in any of them, you're not "at risk" of being shut down — you're shut down by default the moment they figure out what you sell.

3. The Problem With Traditional Processors

Even when a high-risk merchant manages to get approved by Stripe, PayPal or Square, the relationship is structurally unstable. Five problems show up again and again across every traditional processor:

Account Freezes Without Warning

A single risk-model trigger — a chargeback spike, a fraud-flag from a card issuer, a vague compliance review — and your account gets frozen overnight. Funds are locked for 90 to 180 days while the processor "reviews your business." There's no real appeal, no SLA, and very often no human you can actually reach.

Rolling Reserves of 5-10%

Even when things go well, high-risk merchants typically pay a 5-10% rolling reserve on every transaction, held for 6 months. On $50K/month in revenue, that's $25K-$50K of your own money sitting in a processor's account at any given time.

Heavy KYC and 2-6 Week Approvals

Business registration, processing history, bank statements, beneficial-owner documentation, sometimes a personal guarantee — and after all of it, an underwriting decision that takes 2 to 6 weeks. For new businesses without processing history, the answer is almost always no.

Termination Without Explanation

Processor agreements all contain a clause that lets them terminate the relationship at any time, without cause, with 30 days notice. For high-risk verticals, this clause gets used routinely.

Restricted Payment Methods

Most high-risk merchant accounts are limited to basic Visa/Mastercard processing — no Apple Pay, no Google Pay, no alternative methods. In 2026 that means leaving 20-30% of revenue on the table simply because the processor refuses to enable modern checkout flows.

Hard numbers: Internal reports from high-risk merchant communities suggest more than 60% of high-risk businesses have had at least one merchant account terminated within their first 24 months of operation. That's not a tail-risk — it's the baseline scenario.

4. Top 5 High-Risk Payment Gateways in 2026

These are the 5 gateways high-risk merchants are actually using in 2026. They're ordered from the most flexible (no merchant account required, no KYC, instant approval) to the most traditional (full underwriting, dedicated account manager).

1. Chain2Pay — Card-to-Crypto Gateway

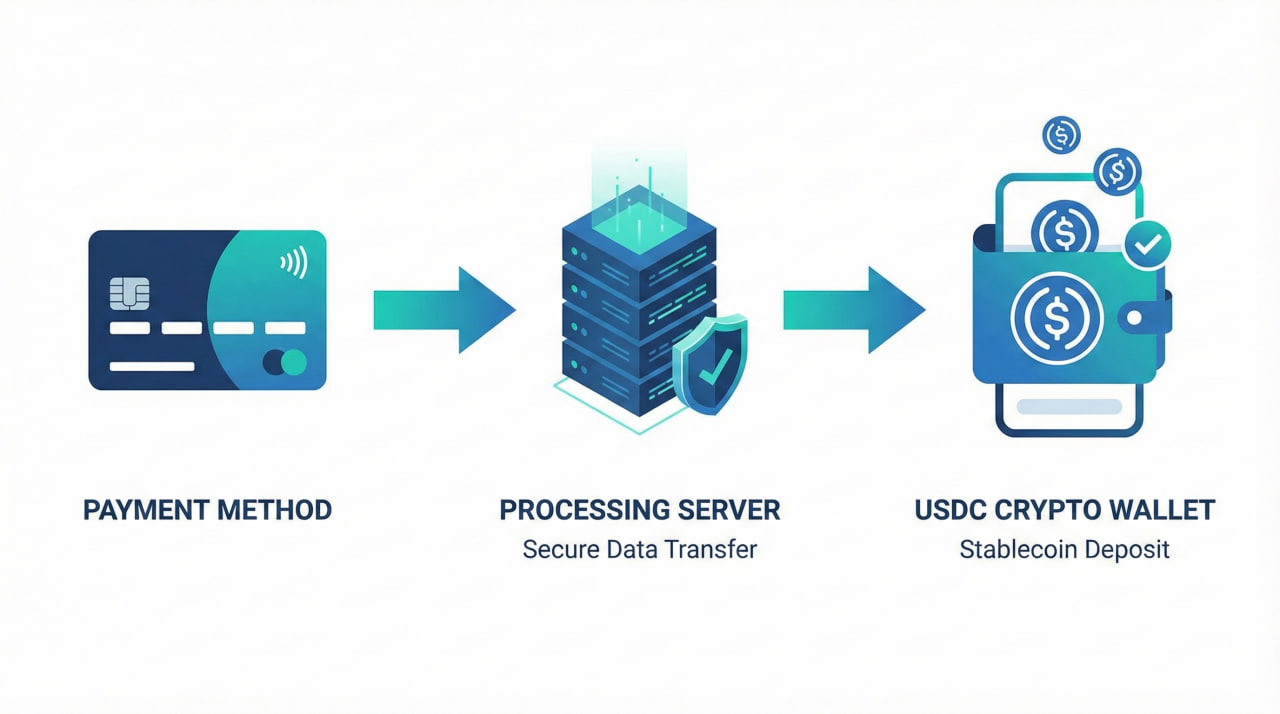

Card-to-crypto gateway. Customers pay with Visa, Mastercard, Apple Pay or Google Pay — the merchant receives USDC on Polygon instantly in a non-custodial wallet. No KYC, no merchant account, instant approval in about 2 minutes. 18+ active providers under the hood, official WooCommerce and WHMCS plugins, REST API v2 with HMAC-signed webhooks.

Fees start at 2.5% on the VIP plan. Works out of the box for IPTV, adult, online gambling, forex, crypto services, SaaS, digital goods and CBD. Settlement is verifiable on PolygonScan in real time. chain2pay.cloud

Key advantage: No merchant account to terminate. Funds settle directly into your own crypto wallet — no intermediary, no acquirer, no processor can ever freeze them.

2. PaymentCloud — Traditional High-Risk Processor

US-based traditional high-risk processor with a dedicated account manager and standard Visa/Mastercard processing on a real merchant account. Serves a wide range of legal high-risk verticals (firearms accessories, e-cig, nutraceuticals, debt collection, etc.). Full KYC and business documentation required, approval typically takes 1-2 weeks. Fees vary heavily by vertical and processing volume — usually disclosed only after the underwriting interview.

3. Durango Merchant Services — Specialist Acquirer

Specialized in high-risk for over 20 years. Card processing, ACH, international payments and offshore acquiring relationships for merchants other processors won't touch. Strong in adult, dating, debt consolidation and travel. Full KYC and complete documentation required. Pricing is custom and is generally on the higher end given the verticals served.

4. NMI (Network Merchants Inc.) — Pure Gateway

Pure payment gateway with high-risk support delivered through a network of partner banks. Very API-focused — ideal for development teams that want a custom checkout and tight programmatic control over the flow. KYC and underwriting are handled separately by whichever partner bank ends up acquiring the merchant, which means timelines and pricing depend entirely on that downstream relationship.

5. NOWPayments — Crypto-Only

Crypto-only payment gateway. Accepts 200+ cryptocurrencies with no KYC required for the base tier. The catch: there is no card processing — customers must already hold crypto to pay. A solid choice for crypto-native businesses (NFT projects, DeFi tooling, Web3 SaaS) whose audience already operates in crypto, but a non-starter for any business that depends on credit card revenue.

5. How to Choose the Right Gateway

Not every high-risk merchant has the same priorities. Before picking a gateway, run through these 7 evaluation criteria — they're the ones that actually matter once you're in production:

- Approval time — minutes, days, or weeks? If you need to start collecting tomorrow, traditional underwriting is a non-starter.

- Transaction fees — flat or per-vertical? Make sure to ask about hidden chargeback fees, monthly minimums and gateway fees, not just the headline percentage.

- Chargeback exposure — does the gateway's model expose you to traditional Visa/Mastercard chargebacks, or does crypto settlement remove that liability?

- Supported payment methods — Visa and Mastercard are table stakes. Apple Pay, Google Pay and PayPal can add 20-30% to conversion on mobile.

- Payout speed — instant settlement (crypto), T+1 (some gateways), or weekly batches with a 6-month rolling reserve (most traditional acquirers).

- Integration options — no-code payment links, REST API, official WooCommerce / WHMCS / Shopify plugins. The closer it fits your existing stack, the faster you ship.

- Customer support — 24/7 live chat, dedicated account manager, or just a ticketing system that takes 4 days to reply.

| Gateway | Approval | Fees | Chargebacks | Payout |

|---|---|---|---|---|

| Chain2Pay | ~2 min | From 2.5% | None (crypto) | Instant USDC |

| PaymentCloud | 1-2 weeks | Custom | Standard exposure | T+1 / weekly |

| Durango | 2-4 weeks | Custom (high) | Standard exposure | Weekly + reserve |

| NMI | Depends on bank | Gateway + acquirer | Standard exposure | Depends on bank |

| NOWPayments | Instant | ~0.5% | None (crypto) | Instant crypto |

6. Why Card-to-Crypto Wins for High-Risk Merchants

Of the 5 models above, card-to-crypto is the only one that structurally solves the problems traditional processing creates for high-risk merchants. Once you remove the merchant account from the loop, every downstream issue disappears with it:

- No merchant account to terminate: there is no Stripe-style relationship that can be revoked. Funds land in your wallet on settlement.

- Zero rolling reserves: 100% of the settled amount is liquid the moment it arrives.

- Instant, irreversible settlement: USDC arrives within minutes, on-chain, verifiable on PolygonScan.

- Global by default: any customer with a card and an internet connection can pay. No country whitelisting, no acquirer geographic limits.

- No chargeback exposure on your side: the fiat side is handled by the acquiring partner; your crypto settlement is final.

- 2-minute setup, no KYC: connect a Polygon wallet, generate an API key, start charging cards.

Chain2Pay is the reference implementation of this model in 2026. It runs the full card-to-crypto flow under the hood, abstracts the underlying acquirer network behind a single API, and gives the merchant USDC on Polygon as the only settlement currency they ever have to think about.

Key advantage: Card-to-crypto eliminates every account-freeze and chargeback risk because there is no merchant account in the loop — funds settle directly in your non-custodial wallet, the moment the card payment is approved.

7. Frequently Asked Questions

Are card-to-crypto gateways legal?

Yes. Card-to-crypto gateways operate within legal frameworks in most jurisdictions. The card processing is handled by licensed acquiring banks, and the crypto settlement is a standard crypto transfer.

Can my customers pay without knowing it's crypto on the backend?

Absolutely. Customers see a standard card checkout. The crypto conversion happens entirely on the backend — they never interact with cryptocurrency.

How fast are payouts with Chain2Pay?

Instant. Once the card payment is approved, USDC arrives in your wallet within minutes. Every transaction is verifiable on PolygonScan.

Do I need a bank account?

No. Chain2Pay requires only a Polygon wallet address to receive funds. No bank account, no KYC, no lengthy application.

Which industries does Chain2Pay support?

IPTV, adult content, online gambling, forex, crypto services, SaaS, digital goods, CBD, peptides, supplements, and most other high-risk verticals.

8. Conclusion

The 5 gateways covered in this article are all viable solutions depending on what you sell, how fast you need to start, and how much friction you're willing to absorb at onboarding. PaymentCloud, Durango and NMI still make sense for established US merchants comfortable with full underwriting and a 1-6 week approval cycle. NOWPayments is the right call if your customers already pay in crypto.

But if you're looking for the fastest path to live payments, no risk of account termination, and instant settlement that no intermediary can freeze, the card-to-crypto model is the clear winner in 2026 — and Chain2Pay is the cleanest implementation of it on the market.

Connect a Polygon wallet, ship a payment link or integrate the REST API in an afternoon, and start collecting Visa, Mastercard, Apple Pay and Google Pay payments with zero chargebacks and instant USDC payouts. That's the new baseline for high-risk processing.